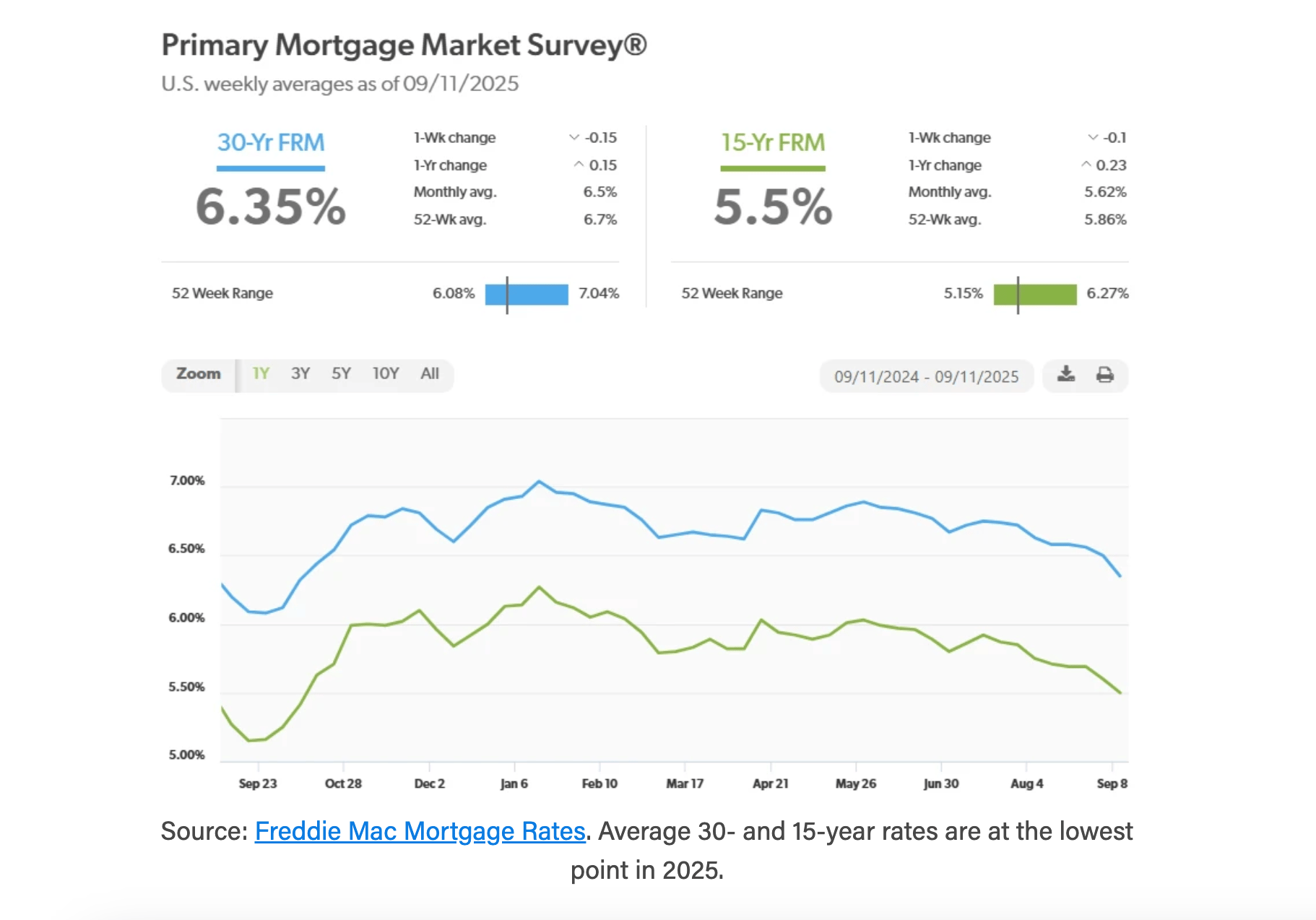

In early September 2025, mortgage interest rates, especially for 30 year fixed loans, began trending downward nationally, moving from mid August levels in the 6.50%–6.60% range toward around 6.35% by mid September. In Colorado, the pattern is similar though rates have generally run a bit higher than the national average. Around September 12, the 30 year fixed rate for purchases in Colorado was approximately 6.61%. Interestingly, in Boulder, some borrowers are seeing rates closer to 6.23% for 30 year fixed rate mortgages which may reflect localized lender competition, stronger borrower credit profiles, or lower margin / fee structures.

Photo credit: Freddie Mac

What this means locally: for Boulder homebuyers, that rate difference of ~0.3-0.4% compared to the broader state average can translate into meaningful monthly savings on a large mortgage, that difference might reduce monthly payments by several hundred dollars. Given that home prices in Boulder are near $940,000, even modest rate drops can improve affordability, or at least reduce the severity of the payments. Meanwhile, in the broader Colorado market, with prices being somewhat lower than Boulder but still high relative to many other parts of the country, falling rates offer relief but may not completely offset the cost pressures from high home prices and elevated down payments.

Regarding Denver, mortgage rates are tracking closely with statewide averages, hovering in the 6.5–6.6% range for a 30 year fixed loan as of mid September 2025, with some local lenders offering slightly better deals in the low 6s for well-qualified buyers. That’s a small but welcome shift from the higher rates earlier this summer, and it’s starting to make a difference in the market. Home prices in Denver have cooled, with the median sitting around $561,000, down nearly 5% year-over-year. Homes are also spending more time on the market, averaging about 35 days which gives buyers more leverage than they’ve had in years. With inventory up, sellers are having to price more competitively and even offer concessions to attract offers.

Additionally, the recent dip in rates is nudging some buyers back into the market, especially those who had been waiting for even a little relief on monthly payments, while refinancing activity has also picked up. Overall, Denver and Boulders markets feel more balanced than it has in a long time, with buyers finally getting some advantages and sellers needing to adjust expectations.